Wheat fell 29% and nobody saw it coming. A 13-week forecast did.

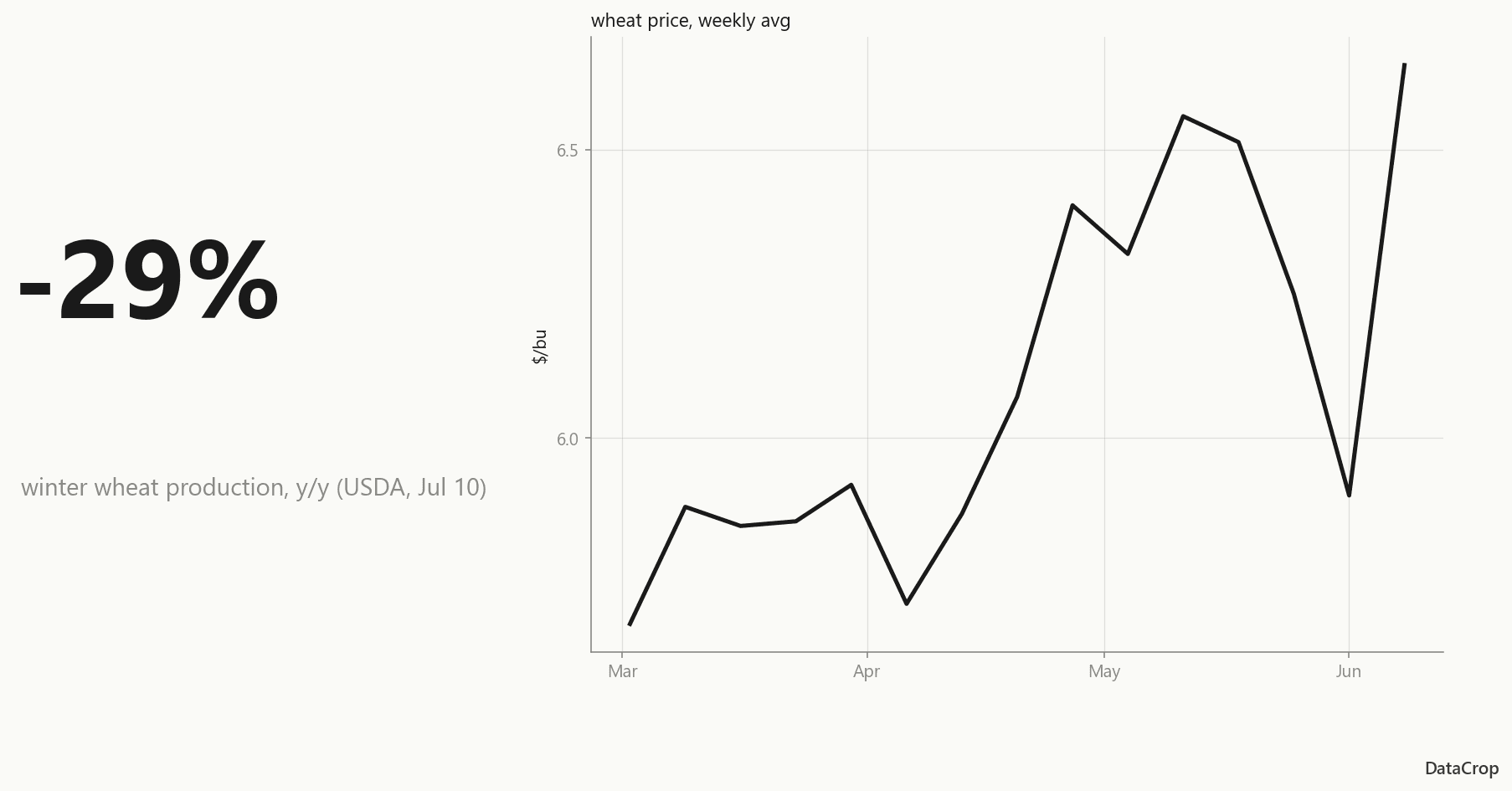

On July 10, USDA confirmed winter wheat production fell 29% year over year - the kind of move that torches a food manufacturer's margin plan. The signal was in the public data by spring.

On July 10, USDA's WASDE report confirmed what wheat buyers had been feeling in their invoices for months: winter wheat production fell to 990 million bushels - down 29% year over year - and the projected farm price climbed $0.94 to $6.00 per bushel.

If you buy flour, that's not a statistic. That's your margin plan on fire.

Here's the uncomfortable part: the signal was in the public data by spring.

What the data showed, month by month

The decline didn't arrive on July 10. It assembled itself in plain sight:

- April: Drought conditions across the southern Plains were already degrading crop-condition ratings. Planted-area numbers from USDA's March intentions report were down.

- May: The first WASDE with 2026/27 projections put winter wheat production well below trend. Regional AMS bids started firming.

- June: Condition ratings kept sliding. The June WASDE trimmed production again.

- July 10: The 'historic decline' headline - and a $6.00 farm price that buyers who waited are now paying.

Each of those data points is free and public. The problem was never access. It's that turning FRED series, NASS QuickStats, and AMS bid reports into a forward view is a part-time job - one to four hours a week that most procurement teams don't have.

What the model's inputs were already showing

An honest disclosure before this section: we haven't yet exported our April model snapshots into a publishable audit trail, so you won't see an 'our April forecast' chart here. (Building that public audit trail is exactly what our WASDE Watch series is for, starting in August.)

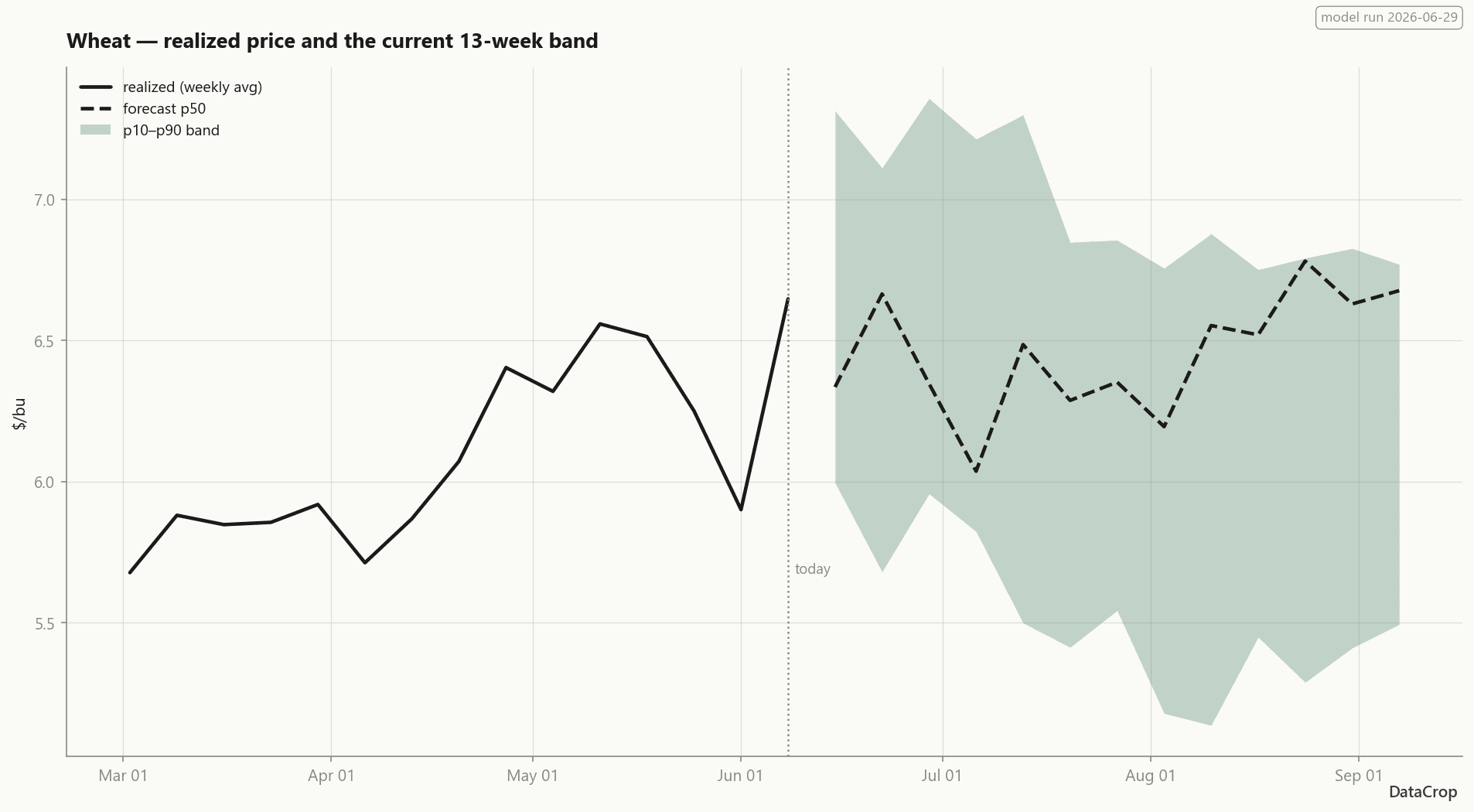

What we can show is what the model's inputs - all public - looked like in April: the crop-condition series in its feature set were degrading week over week across the southern Plains, March planted-area intentions were already down, and the AMS regional bid series were firming. That combination is the textbook shape of a drought year, and it's the kind of input pattern that widens a quantile model's upper band well before the median moves. We're deliberately not claiming a specific April number we can't yet show you - when the audit trail ships, you'll be able to check every historical call yourself.

We won't pretend the model called the exact print. Quantile forecasts don't work that way - and any vendor showing you a perfect historical call is showing you the one chart that worked. What a 13-week band gives you is earlier, quantified asymmetry: the point where 'likely' stops meaning 'stable.'

The buyer math

Say you buy 100,000 bushels a quarter. A buyer who locked at April spot prices versus one who bought through the spring rally paid on the order of tens of thousands of dollars less for the same wheat - the difference between reading a forward band and reading last month's invoice. Run your own volume through the July numbers ($6.00 projected farm price, up $0.94 year over year) and the arithmetic gets uncomfortable fast.

How to read a band like a buyer

A 13-week quantile forecast has three lines:

- p50 (likely): the middle of the distribution - your budgeting number

- p10 (best case for buyers): prices only fall below this 1 time in 10

- p90 (worst case): prices only exceed this 1 time in 10

When the p90 edge starts pulling away from p50, the model is telling you upside risk is building - that's a lock signal, even when the p50 looks calm. That pattern is exactly what drought years produce.

What the model did not do

Honesty section, because it's the whole brand: our point forecast does not beat a naive 'last price' baseline right now - at 1-week horizons it's roughly on par, and even at 13 weeks the naive baseline is hard to beat on raw MAE. We show that skill-vs-naive number in your dashboard, in red, whenever it's negative. What the 13-week forecast adds isn't a sharper point estimate - it's the shape of the band: when conditions shift fast, the p90 edge widens before the p50 moves, so the model says 'less certain' before it says 'higher.' That asymmetry - not a headline accuracy number - is the buy-timing signal, and it's where contracts and budgets live.

The same forecast, free, every Monday

The 13-week wheat and corn forecasts run every week and land in inboxes Monday at 7am ET. One commodity, free, no credit card. If this April had a Monday Number in it, would your Q3 flour costs look different?